The below quote is from a book written in 1931 which has now achieved cult status. I have been researching the German hyperinflation period post WWI in order to get some idea as to how to survive investment-wise were such a hyperinflation to befall the US.

“On the afternoon of July 31st, 1914, the Reichsbank, on its own initiative, suspended the conversion of notes, which in the previous days had come, in great quantities, to its branches to be exchanged for gold. On August 4th the conversion of notes was suspended by law, with effect as from July 31 st… in the two weeks from July 24th to August 7th the quantity of Reichsbank notes in circulation increased by more than two milliard marks. Thus was initiated a monetary inflation that was without precedent in history.”

From The Economics of Inflation – A Study of Currency Depreciation in Post War Germany, Constantino Bresciani-Turroni, p. 23.

Germany During and After WWI – A Lesson in Monetary Inflation

The argument can be made that the German experience is not relevant for the US. Germany after all was the loser in major war and was severely punished in terms of reparations and territorial concessions by the victors. But there just might be some relevance especially when we are evaluating QE2, the expansive US budget deficit and today’s inflationary international monetary system. In fact, the German hyperinflation of 1921-1923 had its roots in massive money printing and debt financing that began when WWI started in 1914. Investment-wise, it’s better to be a citizen of country that is on the winning side of a war. But had Germany won that war, the country would still have been in dire economic straits.

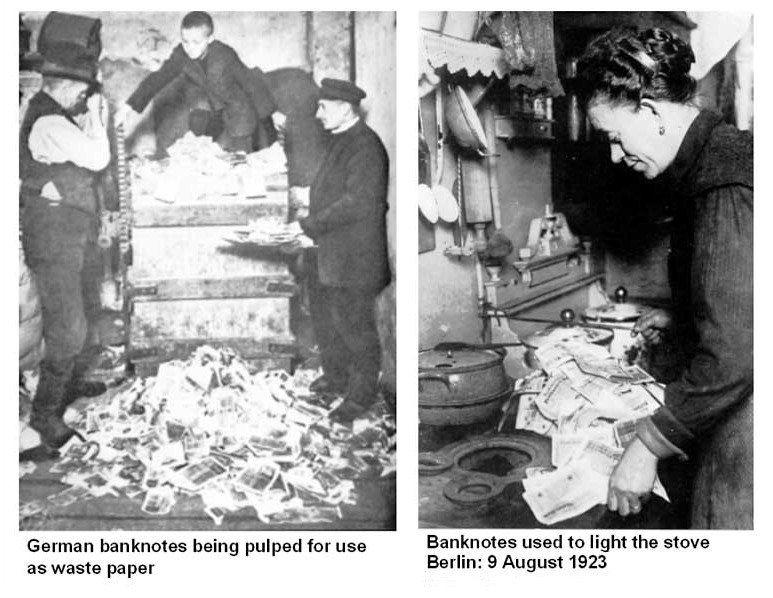

Most investors today are vaguely aware of the German hyperinflation of 1921-1923. They have probably seen the parabolic graph showing German prices going to levels best expressed in exponential terms at the end of the period. They’ve all heard stories of people carrying huge amounts of currency in wheelbarrows just to buy routine items. They probably think that German holders of fixed income securities were wiped out by this incredible hyperinflation as their investments became effectively worthless.

This perception would be slightly off. In fact, by 1921 most of German fixed income holders who had patriotically bought government bonds, mortgages etc during the war were already wiped out largely by the high inflation that cranked up in 1914 and accelerated into the hyperinflationary period beginning in 1921.

Rogoff and Reinhart in This Time It’s Different refer to “default by inflation” as the default method of choice for countries which have over borrowed in their own currency. WWI Germany fit that description. Today the US along with Japan and the euro countries have been borrowing in their own currency with wild abandon. Rogoff and Reinhart define hyperinflation as over 500% per annum. The list of countries that have experienced this extreme version of inflation is longer than you might think. But Rogoff and Reinhart also have compiled a list of countries that have experienced 20%-40% inflation and have therefore in real terms defaulted on debt denominated in their own currency. That list unfortunately is a very long one. A bondholder doesn’t need hyperinflation to go broke. A few years of (unanticipated) 20%-40% inflation will do just fine in terms of seeing his or her investment become worthless in real terms.

From 1914-1921 Germany suffered from accelerating but “only” high inflation. In 1914 when the war began the Reichsbank suspended convertibility of the mark into gold and Germany was taken off the gold standard. (The word “Reich” was still innocent then.) Britain and France also suspended the gold standard. The onset of WWI marked the end of the classic gold standard that had worked so well and had produced near zero inflation for the prior thirty-five years. (The attempt to revive the gold standard in the mid 1920s ultimately proved to be a deflationary fiasco. Like Humpty Dumpty there was no putting the gold standard back together again. But that’s another story.)

To repeat, the German inflationary process began in 1914 when the war began and not in 1918 when it ended. The hyperinflation phase in 1921-1923 was the culmination of this process. German inflation increased steadily from 1914 on as did the depreciation of the mark against the dollar on foreign exchanges. The war was long, costly and financed by massive money printing and borrowing from a clueless if patriotic public. That wasn’t the plan in 1914. The war was supposed to be short, Germany was supposed to win and, as in the Franco-Prussian War of 1871, the hapless losers would pay an indemnity. (The French unfortunately for Germany had a similar plan.) Consequently, the war was financed in Germany not by an increase in taxes but by borrowing and massive money printing. This was a deliberate decision and, like today, there were some people who understood what was happening and opposed it.

The German stock exchange was closed and did not reopen until December 1917. In fact most of the world’s major stock exchanges closed when the war started in the summer of 1914. New York and Paris reopened in December 1914, London in January 1915. Unlike investors who were citizens of their opponents, German investors thus were basically ignorant as to the value of their equity holdings for most of the war. Even when the exchange reopened, in the following years German investors had a hard time evaluating their shares in real terms because of the inflation. Many an investor thought he or she had made money in paper marks when in fact in real terms they were suffering substantial loses in real terms.

A few numbers from Bresciani-Turroni might be helpful. He had several choices in measuring the inflation, i.e., domestic price data, gold as the reference point or the dollar/market exchange rate. He used all three. The different measures did not always move in exact lockstep in the short run but in the long run they paint the same picture of accelerating inflation and economic ruin. All numbers quoted here are as Bresciani-Turroni presented them and are not always totally consistent from period to period but are indicative nonetheless.

Indexing 1913 to 100, by October 1918 Prices of Goods Produced in Germany and Prices of Goods Imported went to 239 and 214 respectively. Thus a fixed income buyer in 1914 would have seen the real value of his or her investment cut in half in real terms as the war came to an end. The Quantity of Money In Circulation hit an index value 440 by October 1918, suggesting that a future acceleration of inflation could have been expected as money during the war grew over twice as fast as inflation. And accelerate it did. Re-indexing October 1918 to 100, by February 1920 Internal Prices and Prices of Imported Goods exploded upward to 506.3 and 1898.5 respectively. All the while the dollar/mark exchange rate was collapsing as well. Repressed inflation from price controls during wartime no doubt surfaced in 1919. After a period of relative stability in 1920- 1921, helped no doubt by the short but deep Depression of 1921 experienced in the United States, the hyperinflation began. By June 1923 and setting July 1922 to 100, Internal Prices and Prices of Imported Goods hit 18194 and 22496 respectively. The numbers just got worse until the currency reform at the end of 1923.

Investment Survival When You Can’t Trust the Currency

How did German investors survive during 1914-1923? Of course fixed income investors did not survive. The German investing public had never experienced serious inflation for all the years under the gold standard. The world had changed on them. Nobody rang a bell. They got totally blindsided.

Actually the German inflation period should be divided into two phases – wartime and post-war. For both periods the best investment strategy was to buy gold or get money out of Germany into foreign exchange. Of course during the war that was unpatriotic and illegal. After the war that was still illegal as the German government tried to prevent capital flight. Sadly, governments frequently betray their citizens’ trust and obedience to the law and patriotism turn out to be the refuge of wealth destruction.

A second choice was domestic shares. The best that can be said from the German experience is that in high and hyperinflationary periods shares in the very long run can preserve wealth if you can stand the volatility and/or are clever at trading. They can bring huge gains to those who pick the right time to enter the markets. According to Bresciani-Turroni, share prices in real terms were substantially below 1913 levels by the end of the war in 1918. From then on shares had a mixed record. For a time through 1920-1921 shares rose when the mark fell against the dollar in the foreign exchange markets. But then shares (in real terms) collapsed in 1922 and hit a low in October. Buyers prescient enough to buy at the 1922 low could have bought and held and made some 1088 percent on their investment by the high in 1928.(This number comes from Bryan Taylor, Global Financial Data) The large industrial companies had preferential access to credit and heavily invested in plant and equipment during the inflation. When it ended they were in good shape although things turned out less well for financial institutions.

Other investment classes turned in differing results. Residential rental housing was a disaster thanks to government imposed rent controls. On the other hand, land – or anything else – that was mortgaged fared very well as in real terms the value of the mortgages was wiped out. Better a borrower than a lender be.

Welfare Nation, Warfare Nation

The above title was taken from a recent speech by David Stockman, formerly Director of the Office of Management and Budget in the Reagan Administration. The nation he was referring to was the United States.

Right now the most important macro event on the near-term horizon is the scheduled termination of QEII on June 30. QE is an economic mistake. The central bank by manufacturing gargantuan amounts of bank reserves out of thin air and handing it over to the government by buying Treasuries is sowing the seeds for future inflation, “stealing” capital from more productive uses in the economy, lowering future total factor productivity growth and distorting the cost of capital.

In the case of WWI Germany, massive money printing was to satisfy government needs for funds, i.e., wartime expenditures, post-war reparations and then just to keep government expenditures up with the inflation itself. QEII on the other hand is advertized as a macro demand stimulus program, not as a funding source for the government. It is supposed to produce just “a little” inflation.

But is QEII just as advertized? Or has the government, like a new heroin addict that has just taken his first shot, already become hooked on this source of funding? The longer term outlook for the US is for endless massive fiscal deficits caused by cyclical and structural factors. The cyclical factors are the significant fall off in government revenues and the bailouts from the recent Great Recession. The structural factors are the aging of the population and the explosive growth of entitlement programs including Medicaid, Medicare, Social Security and now Obamacare. The possibility is real of an eventual crisis in the government bond market unless the Fed steps in as a buyer. Meanwhile, the US is engaged in no less than three wars in the Middle East. Welfare nation, warfare nation.

It will be interesting to see what reaction the bond, foreign exchange and gold markets will have to the termination of QEII. The markets will be watching the government bond auctions very closely. We will find out if the markets take this as good news – a bad program finally ended – or the dreaded day has come when the Federal Government suddenly has to pay up for its insatiable borrowings.